Capital A Financial Results Third Quarter 2025

Group: - RM305m net operating profit (16x YOY)

Aviation: - EBITDA up 76% YoY to RM1.02b

- 23% EBITDA margin

- Operational CASK down 12% YoY

Cap A Companies: - RM22m PAT, extends profit streak to 4 quarters

KUALA LUMPUR, 28 November 2025 – Capital A Berhad (“Capital A” or the “Group”) today reported its unaudited financial results for the third quarter ended 30 September 2025 (“3Q2025”).

The Group recorded a RM305 million net operating profit (“NOP”)—a sharp improvement from RM19 million a year ago—and an EBITDA of RM1.13 billion on RM5.26 billion in revenue, delivering a profit after tax (“PAT”) of RM66 million for the quarter.

Highlights of the AirAsia Aviation Group

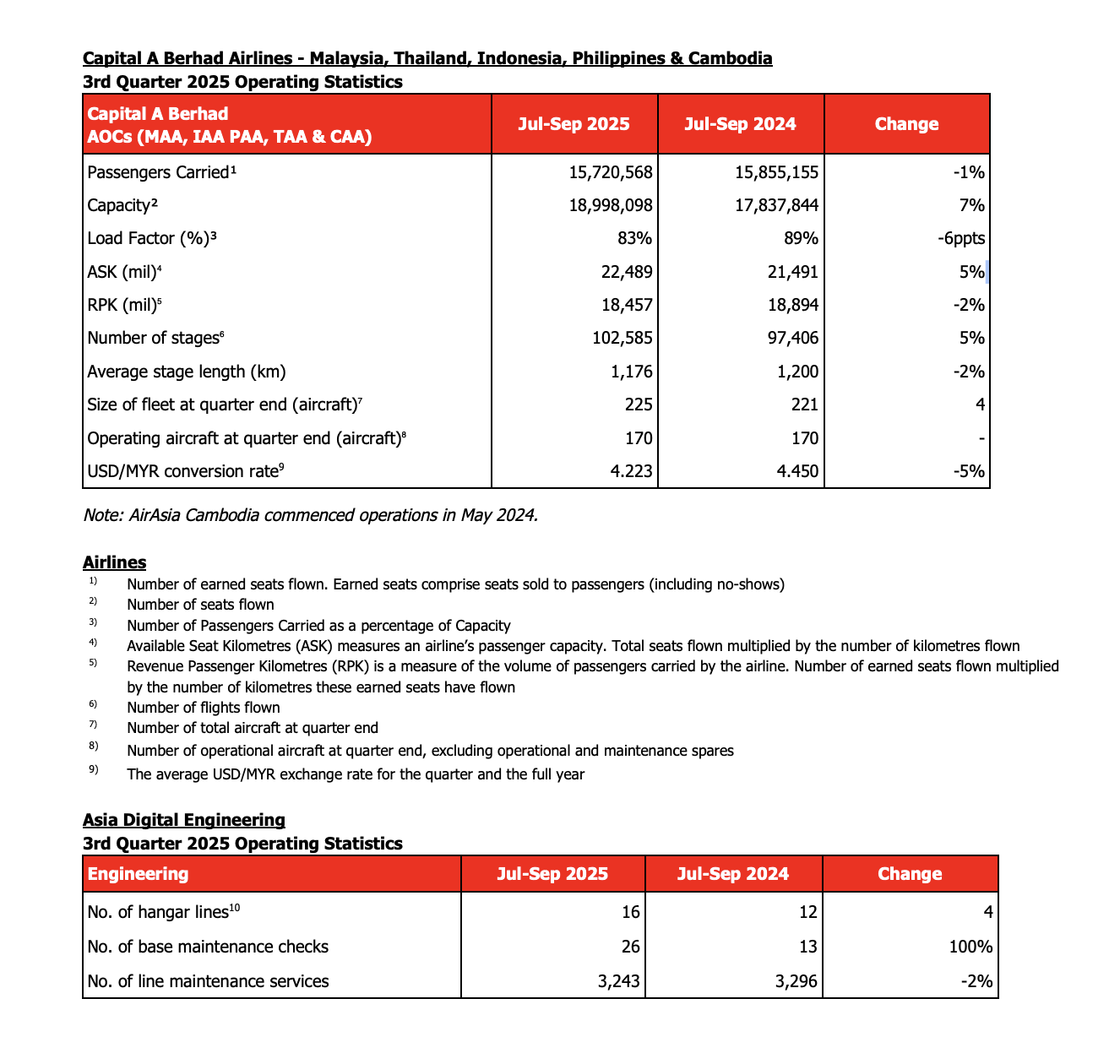

Headline revenue dipped 2% Year-on-Year (“YoY”) to RM4.45 billion, primarily due to continued demand softness in Thailand. Despite marginal topline pressure, EBITDA surged 76% from a year ago to RM1.02 billion, with margin rising 10ppts to 23%, driven by normalisation of maintenance costs, lower fuel prices, as well as ongoing cost optimisation. NOP for the quarter was RM264 million—a turnaround from the RM42 million loss in 3Q2024—with Indonesia and Cambodia turning profitable during the period.

Excluding Thailand, underlying performance remained robust with 3% YoY revenue growth, 30% EBITDA margin and 14% NOP margin, highlighting structural efficiencies built during the pandemic.

Load factor held steady at 83% even with a 7% YoY increase in capacity, which reached 87% of pre-pandemic levels (notably, this was achieved with significantly lower marketing spend of 0.9% of revenue versus 1.5% pre-pandemic)

Average fare and RASK trended lower by 2% and 4% respectively, impacted by Thailand’s shift towards domestic routes to mitigate softer international inbound traffic, though average fare was up 1% YoY across the rest of the network

RM50 ancillary revenue per passenger, with ancillary contribution steady at 18% of AirAsia Group revenue

Operational CASK decreased 12% YoY to USc4.26, largely driven by lower fuel prices and the return to a normalised maintenance profile

Two additional aircraft were reactivated in 3Q25, lifting active fleet to 208 out of 225 aircraft

Group CEO of AirAsia Aviation Group Bo Lingam on the business outlook:

“We expect a strong finish to the year, supported by the seasonal travel surge, a clear rebound in the Thailand market and rising demand from China. By strengthening domestic capacity in Malaysia, Thailand and Indonesia, and accelerating growth in the Philippines, we are already seeing higher loads and stronger ancillary performance. As our aircraft reactivation nears completion by year end, we are fully prepared to enter 2026 with a more productive fleet by growing the network in our core markets with increased frequencies and market share dominance. With our Indonesia and Cambodia businesses turning profitable in 3Q25, we are intensifying our turnaround efforts in the Philippines, which has always been a core market and strategic priority for us.

“As we conclude the aviation corporate restructuring, alongside ongoing progress on debt restructuring, we expect to strengthen our credit profile, lower financing costs and improve liquidity. This will give us the financial resilience to advance our journey toward becoming a narrowbody-driven global low-cost network carrier.”

Highlights of Capital A Companies

On a pre-elimination basis, the Capital A Companies generated over RM817 million in revenue in 3Q2025, up 6% on-year. EBITDA rose 25% YoY to RM113 million, while NOP came in at RM42 million, 31% down YoY mainly on a gain from the remeasurement of interest in the previous year. This drove a PAT of RM22 million, reversing the RM50 million loss from a year ago.

ADE

Revenue rose 20% YoY to RM221 million, driven by a four-line expansion of hangar capacity to 16 lines and a 3% increase in third-party customers during the period. EBITDA strengthened to RM53.5 million from RM29.6 million a year ago, with margin improving 8ppts YoY to 24% on higher maintenance volumes as the enlarged footprint ramped up. Maintenance costs tracked revenue growth, while staff costs grew with personnel transfers from PAA and IAA. Depreciation increased following investments in rotables and tooling, while interest expenses fell as loan repayments progressed from 2Q25.

CEO of ADE Mahesh Kumar on the business outlook:

“This quarter reinforces ADE’s trajectory as a regional MRO leader. Third-party demand continues to grow, and our KLIA expansion plans are moving forward as we secure the financing that will unlock our next phase of growth. Wins like the Air France A330 agreement reflect the trust global airlines are placing in us, underscoring the growing relevance of our capabilities. We’re laying the groundwork for a larger, more competitive ADE, one that will elevate Malaysia’s role in the regional aviation ecosystem.”

AirAsia MOVE

Platform engagement remained healthy in 3Q25, with stable MAUs, steady installs and NPS holding at 57, up 10ppts YoY. Revenue eased to RM112 million from RM129 million a year ago on softer flight volumes due to AirAsia pricing challenges, though this was partly offset by stronger ancillary performance. SNAP and Hotels transactions grew over 40% YoY—with budget-friendly inventory and sharper personalisation driving a 32% YoY improvement in cross-sell rate to Flight users—while Duty Free pre-book conversion nearly tripled on-year to 1.9%. AirAsia Flights held broadly level, recording a modest 2% Quarter-on-Quarter (“QoQ”) increase in GBV and 3% QoQ uptick in bookings despite pricing pressure. Efforts to restore AirAsia Flights price advantage are ongoing, while disciplined cost control kept EBITDA positive at RM12.3 million.

CEO of AirAsia MOVE Nadia Zahir Omer on the business outlook:

“The third quarter underscored the resilience of our model. Despite softer flight volumes, we saw strong momentum across hotels, duty-free and ancillary, validating our budget-first strategy. We continue to build a social-led OTA that drives organic demand at lower cost, reflected in rising engagement, higher conversion and improved NPS. With strengthened partnerships across regional airlines and hotel groups, plus a unified code base lifting speed and efficiency, we’re positioning MOVE to deliver high-quality growth with profitability firmly at the centre.”

Teleport

Teleport reported a net profit of RM8.3 million for 3Q2025, a positive YoY turnaround of RM13.3 million, with management focused on delivering profitability across all levels. EBITDA rose to RM32 million, growing 45% YoY and 28% QoQ, with EBITDA margin expanding 2.4ppts to 10%. This margin improvement demonstrates operating leverage, as growth and control of fixed costs lead to improved profitability. Teleport also delivered its strongest Q3 revenue performance since inception at RM312 million, up 9% YoY and 22% QoQ. Revenue growth was fuelled by a 69% YoY jump in eCommerce revenue to RM116.4 million, delivering a 16% increase in tonnage moved to 90,357 tonnes and a 109% YoY surge in parcels moved to 44.8 million, reinforcing Teleport’s position as the leader in Asean by total tonnage moved by air. Furthermore, the successful SGD51 million refinancing led to a 7% YoY reduction in financing costs amounting to RM630,000, unlocking capital for Teleport to secure strategic long-haul capacity while it concludes its capital raise exercise.

CEO of Teleport Pete Chareonwongsak on the business outlook:

“Our ability to deliver net profitability whilst growing our business by 9% in Q3 validates the resilience of our eCommerce-first strategy, and proves that we can scale profitably. As we close out the year, we will capitalise on our Q3 momentum by focusing on moving more volume out of China through increased capacity and reach of our 50-plus airline partners. Our successful debt refinancing provided the necessary capital to secure capacity for the rest of 2025. The next step for Teleport will be to close its equity capital raise by Q42025 to accelerate our push for global scale (2 million parcels per day), and grow our network beyond Southeast Asia and Asia-Pacific.”

CEO of Capital A Tony Fernandes on the business outlook:

“We built real momentum in Q3, and that puts us in a strong position for what comes next. With the airline disposal nearing completion and PN17 uplift in sight, we are closing the chapter on restructuring and shifting into growth mode.

“What gives me confidence is the progress we’re seeing across the Group. ADE is gearing up to go regional, Teleport is in the top 10 in Asia, MOVE owns the budget OTA space and Santan now serves people on trains. And while it’s early days, AirAsia Next has the potential to become an AI-driven brand and loyalty machine like no other.

“These engines of growth give us real lift as we enter the final stretch of 2025. We’ll continue to sharpen how we operate and be more focused on the opportunities that deliver the biggest impact. Capital A is evolving into something stronger and more valuable and I’m incredibly optimistic about what lies ahead.”