AirAsia X Financial Results Fourth Quarter and Full Financial Year Ended 2025

Enlarged AirAsia X

Enlarged AirAsia X achieves RM1.96 billion Profit After Tax (PAT) for FY25 on a pro-forma basis

Proforma shareholders’ equity of RM767 mil

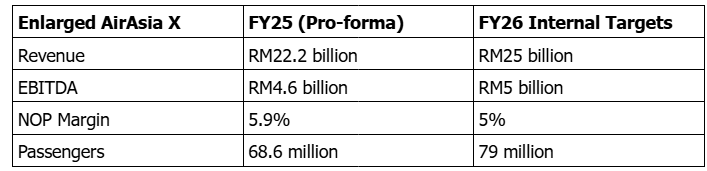

Strategic Outlook: FY26 targets set at RM25 bil Revenue, RM5 bil EBITDA and 5% NOP margin following successful integration

AirAsia X Standalone

AirAsia X PAT reaches RM191.7 million for FY25

4Q25 PAT surges to RM78.6 million, a 3x YoY increase driven by 15% increase in fares as company optimises its widebody operations and foreign exchange gains

AirAsia Short-Haul

Short-Haul Operations deliver a stellar RM500 million Net Operating Profit (NOP), 10% margin, in 4Q25

SEPANG, 26 February 2026 - AirAsia X Berhad (“AirAsia X” or the “Company”) today reported its unaudited financial results for the fourth quarter of 2025 (“4Q25”) and the full financial year of 2025 (“FY25”) ended 31 December 2025, reporting a breakthrough year for its short-haul operations and sustained profitability for its long-haul business.

Following the successful acquisition of AirAsia Berhad and AirAsia Aviation Group Limited, the Group has unified under one single platform (“Enlarged AirAsia X” or the “Group”). To give our shareholders a clear view of our new scale, we are including the full 12-month performance for the short-haul business in this release. This provides a meaningful baseline to evaluate the enlarged platform and bridges the reporting gap to offer a complete view of the assets we brought together as of 16 January 2026.

FY25 Financial Highlights:

On a pro-forma basis, the Group successfully met its profitability commitments, delivering an EBITDA of RM4.6 billion. The Group’s Net Operating Profit (NOP) of RM1.3 billion, with 5.9% margin exceeded internal targets. Revenue for the year was RM22.2 billion, flat YoY, on the back of 2% growth in passenger carried to 68.6 million passengers due to the weak sentiment to Thailand tourism in 2Q-3Q and lower-than-expected number of operational aircraft.

On a standalone basis, AirAsia X concluded FY25 with a Profit After Tax of RM191.7 million on RM3.3 billion in revenue. The Company carried over 4.0 million passengers while maintaining a healthy 82% load factor for the year. Despite higher maintenance costs associated with fleet reactivation and new route launches to Karachi, Tashkent and Istanbul, the Company maintained a disciplined Cost per ASK (CASK) of 13.04 sen, improving 5% YoY.

4Q25 Financial Highlights:

AirAsia’s short-haul operations delivered a stellar 4Q25, achieving a NOP of RM500 million, a significant turnaround from previous losses. This performance was anchored by a strong 84% load factor and a decisive recovery in the Thai market. Notably, Thai AirAsia achieved a significant turnaround to profitability in the final quarter, while associate TAAX delivered its strongest revenue quarter of the year.

AirAsia X Standalone delivered a PAT of RM78.6 million. Performance was underpinned by a resilient fare environment, with average base fares rising 15% YoY to RM568, and forex gains. While seat capacity moderated by 6% due to network realignment, the Company focused on longer-haul services, resulting in a 4% increase in Available Seat Kilometres (ASK). Ancillary revenue grew to RM299.0 million, with spend per passenger rising 13% to RM302.

Operational Excellence:

AirAsia Cambodia Profitability: Proving the power of the brand and network connectivity, AirAsia Cambodia turned profitable in its first full year of operations since its May 2024 launch, achieving a 7.5% FY25 NOP margin

Philippines and Indonesia On Track for Recovery: AirAsia Philippines demonstrates improved EBITDA, with performance set to accelerate via the new Cebu hub and strategic airport partnerships. AirAsia Indonesia remains resilient despite a seasonal weakness in 4Q25, having already demonstrated its earnings potential with a profitable 3Q25.

Cost Leadership: On a pro-forma basis, the Group reduced operating CASK by 9% YoY to 4.26 USc in FY25. This was driven by lower fuel costs, maintenance and user charges, alongside the strategic transition of shorter routes to the narrowbody fleet.

Ancillary Momentum: Spend per passenger reached RM302 for AAX Standalone (up 13%) while remaining a healthy contributor to AirAsia Short-Haul, driven by high take-up in baggage and seat selection via the MOVE platform. On a combined basis, ancillary per pax is RM63 per pax and contributed 19% of revenue.

A New Era:

AirAsia X Group CEO Bo Lingam said, “The successful consolidation of our airlines under one platform is more than just a merger—it’s a homecoming. Our roots are deep in the AirAsia short-haul business that started it all, and we aren't just continuing a legacy; we are evolving it. On behalf of the aviation team, I want to express my deepest gratitude to Tony Fernandes and Datuk Kamarudin Meranun for their visionary leadership and steadfast guidance over the years. We look forward to working even closer with Capital A as strategic partners.

“2025 was the ultimate litmus test. We said we would prove the scalability of our model, and the results speak for themselves. Despite the hurdles of fleet reactivation, we met our internal targets, and our 4Q25 performance—led by a stellar RM500 million net operating profit in short-haul—shows the incredible momentum we are carrying into the new year.

“I am especially proud of AirAsia Cambodia turning profitable in its first full year. I am also heartened by the turnaround in Thailand and the Philippines, where improving sentiment drove Thai AirAsia back to profitability in 4Q25 and achieving EBITDA positive in the Philippines in the year is a huge win. Indonesia has already proven its ability to swing back to profit as seen in its 3Q25 results.

“Now in 2026, we are doubling down on our efforts to re-establish our position among the world’s lowest-cost airlines to build the world’s first true low-cost network carrier. This is anchored by a stronger balance sheet following our recent RM1.0 billion capital raise and ongoing refinancing exercises. On network, we seek further leadership in our core ASEAN markets while also deepening our reach in high-potential growth corridors, supported by our upcoming long-range narrowbody fleet. Establishing Bahrain as our first global hub is a game-changer, allowing us to connect Asia to Europe and the Middle East more efficiently than ever before.

“Operationally, the 'reset' is over and the growth phase has begun. We are shifting from simply reactivating planes to optimising a world-class fleet. With a strengthened balance sheet, we are accelerating our shift to newer, fuel-efficient aircraft and leveraging data to drive down unit costs. In 2026, we target to maintain our fleet size of 253 aircraft as four (4) new A321LR will replace retiring fleet. We are currently in discussions with OEMs to expand our orderbook by up to 150 additional aircraft, on top of the existing 374 aircraft orderbook, to ensure we have the capacity to lead for the next decade. Our mission remains unchanged: democratising air travel and ensuring that now everyone can fly to more destinations than ever before, while delivering long-term value for our shareholders.

2026 Internal Targets:

Armed with an enlarged fleet and a unified strategy, the Group has set bold targets for FY26:

Notes:

Pro-forma financial figures include the 12-month consolidated results of AirAsia Berhad (Malaysia), Thai AirAsia, AirAsia Indonesia, AirAsia Philippines, and AirAsia Cambodia as if the aviation consolidation had been completed on 1 January 2025. This is provided for illustrative and baseline purposes only.

Net Operating Profit (NOP) is defined as earnings from core airline operations before non-operating aircraft depreciation and non-operating aircraft finance costs.